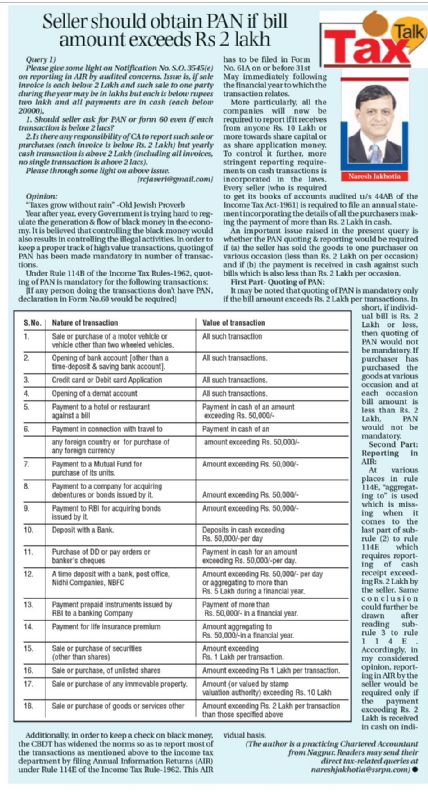

| S.No. |

Nature of transaction |

Value of transaction |

| 1. |

Sale or purchase of a motor vehicle or vehicle other than two wheeled vehicles. |

All such transactions. |

| 2. |

Opening of bank account [other than a time-deposit & saving bank account]. |

All such transactions. |

| 3. |

Credit card or Debit card Application |

All such transactions. |

| 4. |

Opening of a demat account |

All such transactions. |

| 5. |

Payment to a hotel or restaurant against a bill |

Payment in cash of an amount exceeding Rs. 50,000/- |

| 6. |

Payment in connection with travel to any foreign country or for purchase of any foreign currency |

Payment in cash of an amount exceeding Rs. 50,000/- |

| 7. |

Payment to a Mutual Fund for purchase of its units. |

Amount exceeding Rs. 50,000/- |

| 8. |

Payment to a company for acquiring debentures or bonds issued by it. |

Amount exceeding Rs. 50,000/- |

| 9. |

Payment to RBI for acquiring bonds issued by it. |

Amount exceeding Rs. 50,000/- |

| 10. |

Deposit with a Bank. |

Deposits in cash exceeding Rs. 50,000/-per day |

| 11. |

Purchase of DD or pay orders or banker's cheques |

Payment in cash for an amount exceeding Rs. 50,000/-per day. |

| 12. |

A time deposit with a bank, post office, Nidhi Companies, NBFC |

Amount exceeding Rs. 50,000/- per day or aggregating to more than Rs. 5 Lakh during a financial year. |

| 13. |

Payment prepaid instruments issued by RBI to a banking Company |

Payment of more than Rs. 50,000/- in a financial year. |

| 14. |

Payment for life insurance premium |

Amount aggregating to Rs. 50,000/-in a financial year. |

| 15. |

Sale or purchase of securities (other than shares) |

Amount exceeding Rs. 1 Lakh per transaction. |

| 16. |

Sale or purchase, of unlisted shares |

Amount exceeding Rs 1 Lakh per transaction. |

| 17. |

Sale or purchase of any immovable property. |

Amount (or valued by stamp valuation authority) exceeding Rs. 10 Lakh |

| 18. |

Sale or purchase of goods or services other than those specified above |

Amount exceeding Rs. 2 Lakh per transaction |

.png)