.png)

Article Details

| Seller should obtain PAN if bill amount exceeds Rs. 2 Lakh | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

TAX TALK-12.09.2016-THE HITAVADA TAX TALK CA. NARESH JAKHOTIA Chartered AccountantSeller should obtain PAN if bill amount exceeds Rs. 2 Lakh Query 1] Please give some light on Notification No. S.O. 3545(e) on reporting in AIR by audited concerns. Issue is, if sale invoice is each below 2 Lakh and such sale to one party during the year may be in lakhs but each is below rupees two lakh and all payments are in cash (each below 20000),

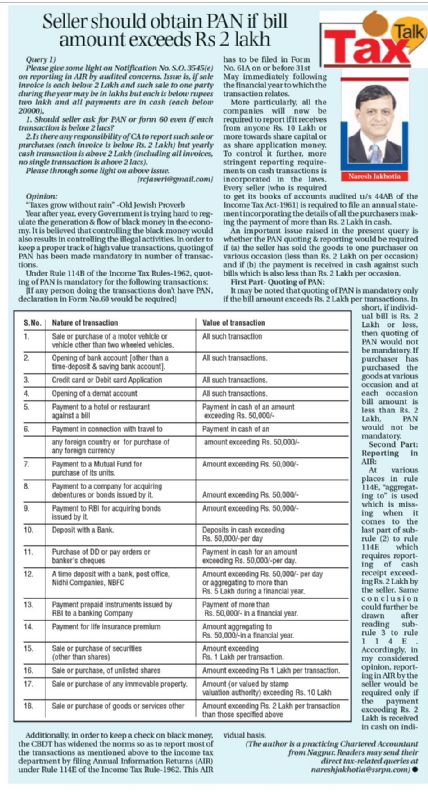

Opinion: “Taxes grow without rain” -Old Jewish Proverb Year after year, every Government is trying hard to regulate the generation & flow of black money in the economy. It is believed that controlling the black money would also results in controlling the illegal activities. In order to keep a proper track of high value transactions, quoting of PAN has been made mandatory in number of transactions.Under Rule 114B of the Income Tax Rules-1962, quoting of PAN is mandatory for the following transactions:

Additionally, in order to keep a check on black money, the CBDT has widened the norms so as to report most of the transactions as mentioned above to the income tax department by filing Annual Information Returns (AIR) under Rule 114E of the Income Tax Rule-1962. This AIR has to be filed in Form No. 61A on or before 31st May immediately following the financial year to which the transaction relates. More particularly, all the companies will now be required to report if it receives from anyone Rs. 10 Lakh or more towards share capital or as share application money. To control it further, more stringent reporting requirements on cash transactions is incorporated in the laws. Every seller [who is required to get its books of accounts audited u/s 44AB of the Income Tax Act-1961] is required to file an annual statement incorporating the details of all the purchasers making the payment of more than Rs. 2 Lakh in cash. An important issue raised in the present query is whether the PAN quoting & reporting would be required if (a) the seller has sold the goods to one purchaser on various occasion (less than Rs. 2 Lakh on per occasion) and if (b) the payment is received in cash against such bills which is also less than Rs. 2 Lakh per occasion. First Part- Quoting of PAN: It may be noted that quoting of PAN is mandatory only if the bill amount exceeds Rs. 2 Lakh per transactions. In short, if individual bill is Rs. 2 Lakh or less, then quoting of PAN would not be mandatory. If purchaser has purchased the goods at various occasion and at each occasion bill amount is less than Rs. 2 Lakh, PAN would not be mandatory. Second Part: Reporting in AIR: At various places in rule 114E, “aggregating to” is used which is missing when it comes to the last part of sub-rule (2) to rule 114E which requires reporting of cash receipt exceeding Rs. 2 Lakh by the seller. Same conclusion could further be drawn after reading sub-rule 3 to rule 114E. Accordingly, in my considered opinion, reporting in AIR by the seller would be required only if the payment exceeding Rs. 2 Lakh is received in cash on individual basis. [The author is a practicing Chartered Accountant from Nagpur. Readers may send their direct tax related queries at SSRPN & Co 10, Laxmi Vyankatesh Apartment C.A. Road, Telephone Exch. Square Nagpur-440008 or email it at nareshjakhotia@ssrpn.com]

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|